How Much Does High Value Home Insurance Cost?

High value home insurance doesn't have a single fixed price. In today’s UK market, many policies for high value homes start from around £2,000 to £3,000 per year, then rise as rebuild values, contents and complexity go up. By contrast, ABI data for 2025 shows the average combined buildings and contents premium is around £390–£400 per year.

What you actually pay for high value home insurance depends on the rebuild cost of the buildings, the value of your possessions, where the insured property’s located and your claims history. The main aim is usually to be properly protected rather than to chase the very lowest home insurance cost.

As an FCA regulated UK insurer focused on high value homes, we're pricing and managing these risks every day, so the information in this guide is based on what is commonly observed across the market.

Typical costs for high value home insurance

For a typical high value home with a rebuild cost close to £1 million and contents worth six figures, it's common to pay in the low thousands per year rather than a few hundred. You're paying for higher limits on buildings cover and contents cover, plus broader coverage than standard home insurance policies tend to offer.

Standard home insurance averages give a useful benchmark. ABI figures show the average combined buildings and contents premium at around £390 a year, while other analysis suggests most ordinary homes still pay under £500 a year. High value homes often pay several times that, because a single insured event could involve a six or seven figure claim.

To anchor it in real life, imagine three households:

- One owns a modern house with a £900,000 rebuild cost and sensible home security; their premium might sit towards the lower end of the high value range.

- Another has a listed townhouse with £1.8 million rebuild cost and £250,000 of possessions; their premium may fall in the mid-thousands.

- A third has an estate with multiple properties and high value items such as jewellery and fine art; they'll usually see fully bespoke pricing.

For many of the clients we speak to at rivr, the key shift is accepting that insurance for a high value home sits in the low thousands rather than the low hundreds, then making sure that extra spend is buying genuinely better protection rather than just a bigger number on the direct debit.

Example premium ranges for high value homes

This table shows, in simplified form, how high value home insurance premiums can scale as rebuild values and contents increase.

These bands are indicative only. They’re loosely scaled from average combined home insurance premiums and then adjusted for the much higher sums insured and policy limits that apply to high value homes and contents. They help show how quickly premiums move once you exceed typical limits.

Many insurers treat you as a high value home client if your valuables together exceed around £50,000, or you own a single piece worth £25,000 or more. At that point, standard limits and single item caps can start to bite.

Specialist insurers like rivr then bring buildings insurance, contents insurance and high value items together under a single high value home insurance policy, rather than leaving you to juggle multiple disconnected policies. With rivr, the aim is to keep that single policy simple to manage online while still giving you the bespoke protection high value homes need.

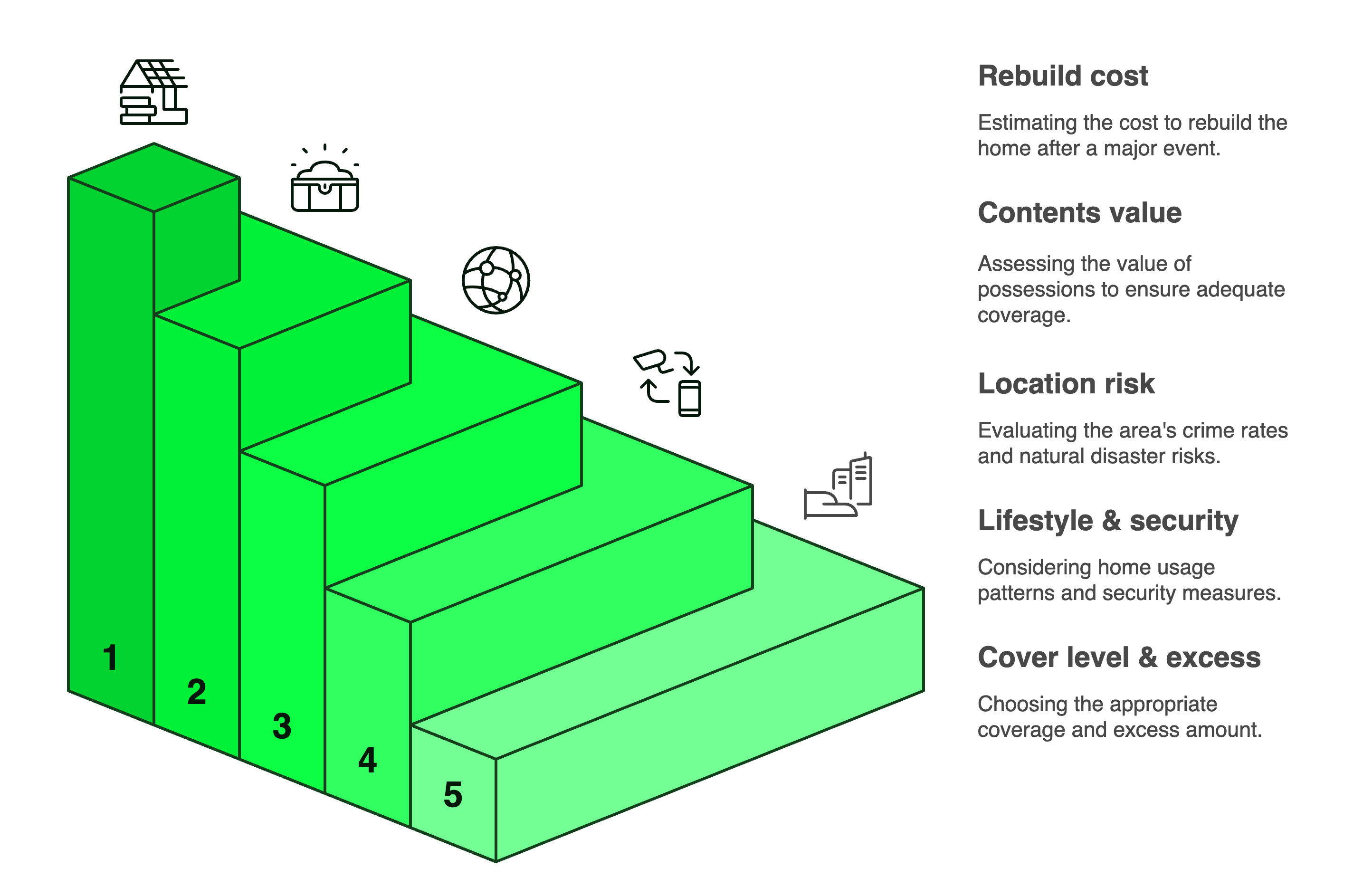

What actually drives the cost of high value home insurance?

Rebuild cost and construction

The rebuild cost is one of the most important factors in pricing high value home insurance. This is the amount it would cost to rebuild the house after a major insured event, including materials, labour, professional fees, and debris removal. It's not the same as market value, which can be higher or lower.

Homes that use specialist materials, have complicated layouts or are listed buildings generally cost more to repair or rebuild. That pushes up the sum insured for buildings and, in turn, the premium. For high value homes, many insurers encourage a professional survey to estimate the rebuild cost, because underinsurance in this area can significantly affect any claim.

When you get a quote from rivr, getting as close as possible to the true rebuild cost helps us design cover that matches the real exposure, not just what happens to be in a price comparison dropdown.

Contents, valuables and collections

The second major driver is the value of your possessions. Standard home insurance only fully protects contents up to a certain level, and often has relatively low limits for high value items. High value contents cover's aimed at households with expensive jewellery, family heirlooms, art or collections that wouldn't be adequately covered under basic limits.

You may step into high value home insurance territory if your combined valuable items exceed about £50,000, or you own a single piece worth £25,000 or more. In that case, you'll often have a schedule of specified high value items, and the insurer may ask for valuations so any damaged items can be repaired or replaced accurately if you claim.

With rivr, your contents are insured up to £500,000 and you only need specify individual items over £25,000.

Location and risk factors

Location's a third core factor. Insurers look at crime levels, local claims patterns and flood or subsidence maps when they price home insurance policies. Flood Re, the government backed reinsurance scheme, was created to help insurers keep flood cover available and more affordable for households at high flood risk, but premiums in those areas can still be higher than the UK average.

If an address has a long claims history, for example repeat escape of water or a past oil leak from heating, insurers will take that into account. A high value home in a very low crime, low flood risk area may attract a more favourable premium than a similar property with more risk factors in play.

Lifestyle, security and usage

How you use the home also affects what you pay. A lived in family home that’s occupied most of the time presents a different risk to a holiday home that can stand empty for months. Longer unoccupied periods, extensive outdoor areas such as pools, or frequent visitors can all change risk.

Insurers ask about home security because it reduces the chance of theft and some types of damage caused by intruders. Alarms, locked gates, safes for jewellery and prompt repair of any broken lock all help improve the security picture. That may not guarantee a lower premium, but it can support higher limits or more flexible coverage for high value contents.

When we look at a high value property, good security and sensible risk management often give us more room to offer the kind of broader cover high net worth clients expect.

Cover level and excess

Finally, the level of cover and the excess you choose also influence cost. Many high value home insurance policies include accidental damage on buildings and contents, higher alternative accommodation limits, home emergency assistance and family legal expenses. These features increase financial protection, but they also increase premium compared with a basic policy that strips them out.

You can usually choose a voluntary excess. A higher excess means you pay more yourself when you claim, so the insurer’s costs are lower and the premium can fall. The trade off is that a very high excess can make smaller claims unattractive, so it's important to choose a level that fits the way your family would want to use the home insurance policy in practice.

With rivr, it's straightforward to model different excess levels and see how they change your premium, so you can decide where that balance sits for you.

Why high value home insurance costs more than standard cover

High value home insurance costs more than mainstream products because it's built for properties and possessions that sit beyond standard home insurance cover. It’s specialist cover that protects expensive property and possessions with high limits and comprehensive protection commonly included.

High value home insurance often includes:

- Higher sums insured for buildings, contents and single items than standard home insurance policies allow

- Wide coverage, for example all risks worldwide cover on possessions and generous alternative accommodation limits

- Support for complex claims, such as reinstating listed features or conserving fine art

Instead of simply increasing the price, these products reshape the coverage so that one serious claim doesn't leave a shortfall. That’s why, for many customers, the key question isn't only the price but whether the high value home’s fully protected if something significant goes wrong.

At rivr, our focus is on making that kind of specialist cover feel as simple as a standard policy to buy and manage, while still behaving like a true high net worth product when you need it.

How to keep premiums competitive without undercutting cover

Modern guidance on cutting home insurance cost usually focuses on two things: better information and better risk management. Both apply strongly to high value homes.

1. Nail down accurate numbers

A professional assessment of the rebuild cost, plus a room by room list of possessions and high value contents, gives a clearer picture of what needs to be insured. This reduces the risk of underinsurance, but also avoids paying for cover you don't need if your original estimates were too high.

If you choose to insure with rivr, coming to us with recent valuations and a realistic contents estimate helps us get your cover right from day one.

2. Think about practical risk reduction

Simple steps like improving home security, keeping roofs and plumbing in good condition, lagging pipes and installing leak detection systems all reduce the likelihood and severity of claims. For a high value home, that might also include extra fire protection around plant rooms or specialist storage for fine art and wine.

These measures won't remove risk, but they can influence how insurers view it. Insurers may look positively on homes where clients have clearly invested in reducing obvious risks.

3. Consider how your insurance policies are structured

Some high value homes benefit from combining buildings cover, contents cover and cover for high value items under one high value home insurance policy, sometimes across several properties. Others still prefer separate policies for a main residence and a holiday home. A specialist insurer may be able to help you compare options and find the right cover for the way you live.

With rivr, you get a single digital policy that can cover high value buildings, contents and valuables together, instead of multiple overlapping contracts.

4. Model different excess levels with your insurer

Seeing how much the premium changes for a £500, £1,000 or £2,500 excess helps you decide where the balance between day to day costs and long term financial protection.

What a specialist will ask before giving you a price

Before an insurer can provide an accurate home insurance quote for a high value home, they need enough information to understand the risk properly. That usually means a slightly deeper questionnaire than a standard price comparison, but most of it’s straightforward.

The key questions you’ll be asked

rivr: cover for those with more to protect

rivr is a digital-first high value home insurance provider. We tailor home insurance policies that bring together buildings, contents, fine art, property emergency and family legal expenses under a single digital contract. These include cover up to £3 million for buildings and £500,000 for contents and valuables, subject to underwriting.

If you're considering high value home insurance for the first time, gather any rebuild estimates, contents lists and recent claims details, then start a quote with rivr. You can see how the premium looks in practice, adjust cover and excess levels in real time, and be confident you are paying the right price for the right protection.

Read more

Frequently asked questions

High value home insurance is typically designed for situations where a single loss could involve rebuilding a high value home and replacing high value contents at a level that may exceed the limits of standard policy. Whether it is suitable depends on the property, the value of possessions and the level of risk exposure. Insurers, brokers and policy documents can explain the type of cover provided and how it differs from standard policies.

There is no single legal definition. But, many insurers and brokers often use markers such as:

- A rebuild cost approaching or exceeding certain thresholds (e.g., around £750,000 or higher).

- Contents worth over £100,000.

- Individual valuable items above insurer-specific limits, for example £25,000 for a single piece or £50,000 in total.

Listed buildings, properties with non-standard or specialist construction, extensive collections (e.g., fine art, antiques), or multi-building sites may also fall into categories treated as high value by insurers. These thresholds vary between providers.

Yes. Some home insurance and high net worth products allow you to insure more than one property, such as a main residence and a holiday home, under a single policy. This can reduce admin and help the insurer understand your total risk. Other insurers may provide separate policies for each property. The structure depends on the insurer’s product design and underwriting approach.

Many insurers recommend reviewing the sum insured for both buildings and contents regularly (commonly on an annual basis), and whenever something significant changes. This includes major building work, large purchases of high value items or art, or changes to how the property is used. With construction costs and materials prices moving quickly, using outdated figures may increase the risk that the sums insured do not match current costs.

The cost of high-value home insurance depends on a number of factors such as the amount of cover required, and other risk factors such as flood or theft risk.

Premiums are usually higher than standard insurance because of the increased value and risk, but with this premium, you receive broader and more extensive cover with higher limits than is available with standard home insurance.

The policy is insured by two of the largest insurance companies in the world, which are both A- rated for their financial strength. The Buildings, Contents and Liability cover is insured by Accelerant Insurance UK Limited. The Property Emergency and Family Legal Soluations are insured by ARAG Legal Expenses Insurance Company Limited.

Rivr can insure Grade II* and Grade II listed homes in England and Wales, and Category B and C listed properties in Scotland, subject to underwriting review.