.jpg)

High Value Home Insurance: Complete Guide for UK Homeowners

High value home insurance serves households where the rebuild cost, collections or lifestyle exceed a standard policy. It widens protection, simplifies schedules and recognises complex properties. rivr focuses on primary residences for high value homes and arranges clear buildings and contents terms within one home insurance policy for customers who want clarity and speed rather than a traditional broker. Use this guide to set each sum insured correctly, compare options and choose the right cover without guesswork.

What is high-value home insurance?

High-value home insurance is specialist cover for properties with exceptional rebuild costs, distinctive architecture, or valuable contents. Broadly speaking, it's a type of home insurance suited to luxury apartments, large family homes, listed or architect-designed buildings, and houses built with rare materials.

In the UK, a high-value home is often defined by a rebuild cost of around or above £1 million. Rebuild cost is the price to rebuild the property from the ground up with like-for-like materials and standards. If your home would cost £1.5 million to rebuild, you need cover set to that figure rather than a market value.

When you might need specialist cover

Use this as a quick sense check.

- Rebuild cost around or above £1 million, or far above local norms.

- If you own fine art, watches, jewellery, or collections that what is generally accepted on standard policies - about £30,000

- Listed status, period details, bespoke materials, or complex construction.

- High-spec features such as an indoor pool, extensive outbuildings, or tennis courts.

- Non-standard occupancy. Holiday lets, long absences, multiple homes, or paying guests.

- Major renovations planned or ongoing.

- Need for higher liability limits or worldwide protection for valuables.

Specialist policies typically provide higher limits, broader contents protection, and fewer restrictive conditions. They can consolidate buildings, contents, and valuables on one policy to reduce gaps at claim. Share unusual features and security details early so sums insured and terms are accurate.

Set your buildings sum insured using rebuild cost

For high value home insurance and specialist insurance, set the buildings sum insured by rebuild cost, not market value or net worth home insurance. The aim is a like for like reconstruction figure.

Include demolition and site clearance, professional fees for architects and engineers, building regulations and compliance upgrades, and fixed services and outbuildings. Many insurers index link using the BCIS House Rebuilding Cost Index.

The BCIS public calculator can help you sense check, but it is a guide, not a survey. Be careful when considering the quality of finish of your home, as this is a big driver to your rebuild cost.

If a mortgage valuation understates the rebuild cost, commission a professional assessment. Revisit the sum insured after renovations or new purchases rather than waiting for the last five years.

Accurate sums insured support settlement up to the maximum value allowed by your policy wording after an insured event. Set separate contents sums for valuable possessions and consider worldwide cover for personal items so they remain fully protected. Check your home insurance policy for limits and exclusions.

Practical steps to choose the right cover

- Commission a rebuild assessment that includes external walls, garages, and outbuildings.

- Itemise high value contents room by room and attach current valuations for high value items and fine art.

- Record new purchases and update the sum insured at renewal so you stay properly covered.

- Confirm index linking and review sums every couple of years in a fast moving market.

- Check alternative accommodation cover limits and any automatic cover for new purchases between valuations.

- Add accidental damage and home emergency cover if needed.

- Review single item limits, specify valuable items, and place personal items on worldwide cover where required.

Typical features of a value home insurance policy

How claims work: step by step

If an insured event occurs, make the home safe, tell your insurer promptly, and keep clear evidence. The exact steps and limits sit in your home insurance policy, so check the policy wording and your schedule for sums insured, exclusions and any endorsements.

- Make safe and mitigate: Turn off water, gas or electricity if needed. Prevent further damage and keep receipts for urgent work.

- Notify quickly: Report the claim as soon as possible with policy number, date, cause and what was damaged. For theft, attempted theft or vandalism, notify the police and obtain a crime reference. Do not admit liability.

- Record the loss: Photograph damage, keep damaged items, list losses with values, and gather invoices, valuations and guarantees.

- Assessment: Your insurer may request estimates, send a claims handler or loss adjuster, or appoint authorised repairers to make safe and manage repairs.

- Alternative accommodation: If the home is uninhabitable after an insured event, alternative accommodation cover may apply. Check duration, caps and what costs are included.

- Settlement: Insurers settle by repair, replacement or cash, subject to the sum insured and any excess. Treatment of pairs and sets varies. Time limits often apply for newly acquired possessions notifications.

- Aftercare and recovery: Co-operate with reasonable information requests. Keep items until the insurer confirms disposal. The insurer may pursue recovery from third parties.

Why high net worth households choose rivr

Collections, valuations and itemising high value contents

High value contents such as jewellery and watches benefit from recent valuations, and fine art often requires specialist reports. List items that breach single article limits and review values after auctions or market changes. Where needed, ask for bespoke cover for antiques or art and check whether extended replacement cover or unlimited cover is available, as well as how pairs and sets are treated within the policy wording.

For broader context on families with complex schedules, Rivr’s guide to high net worth insurance explores who is insured across the household, how personal items are defined, and where a combined approach helps.

Alternative accommodation and living costs after a major loss

If an insured event makes your home uninhabitable, alternative accommodation funds a similar standard of living while repairs take place. For high value homes, rebuilds can take longer, so confirm both duration and any daily limits. Consider pets, schooling and security, particularly where work and study anchor your family to a neighbourhood or across multiple locations.

Look for alternative accommodation cover that matches the area and school catchments you actually use. This practical lens matters more than headline numbers and helps protect continuity if the worst happen.

Escape of water, LeakBot and everyday prevention

Escape of water is a leading driver of claim frequency and cost in UK homes. The ABI explains typical causes and the scale of payouts for water leaks, which underlines why prevention matters and why insurers focus on plumbing resilience. Consider smart monitoring. Some providers supply a free leakbot to existing customers, and LeakBot’s overview explains how continuous monitoring detects leaking water before it escalates.

Early alerts reduce damage caused by damp, warped finishes and mould, and can lower the cost you ultimately pay in reinstatement and disruption. If you suspect a leak, act quickly and keep basic evidence to support a claim.

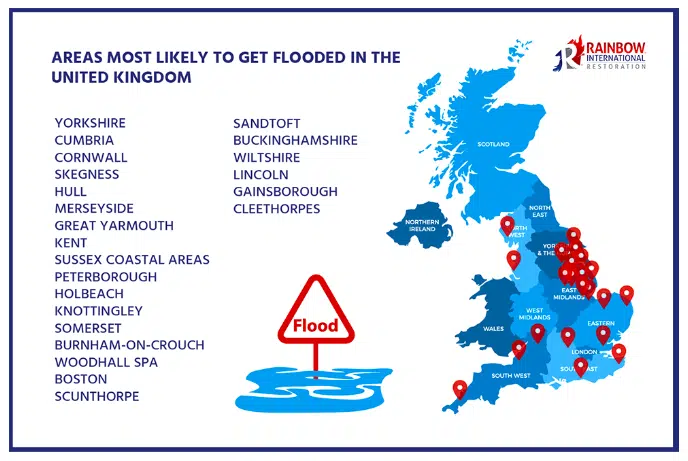

Flood exposure, location and listed constraints

Use the government’s service to check long term flood risk and whether your address sits in flood risk areas with specific defences in place. The tool is free and updates periodically with river, surface water and coastal data. For a deeper view, the ABI explains what a property level flood risk assessment includes and how it informs practical improvements that protect the fabric and services of the home.

Owners of a listed building must follow Historic England’s rules for Listed Building Consent and should share plans with their insurer early so scope, materials and timeframes are understood. Guidance covers interiors as well as exteriors and is a useful reference before commissioning works.

People, occupancy and day to day use

Tell your insurer if you host paying guests, leave the home unoccupied for extended periods or maintain a holiday home. Clarify security requirements and any higher excess that applies during guest stays or while the home is empty. If you look after multiple properties, ask whether one value home insurance policy can capture them under a single relationship and confirm how liability is arranged.

If emptiness is likely during works or moves, our guide to unoccupied home insurance explains common conditions and how to keep home insurance cover valid during longer absences. If you own period features, rivr insures Grade II and II* listed buildings up to £3 million, and above by exception.

How much does high value home insurance cost?

Tips for managing pricing and risks

Price depends on your buildings and contents sums insured, construction, security, claims history, flood mapping and specialist trades. The market tracks inflation in materials and labour that BCIS indices reflect, so index linking helps keep values aligned between reviews. Combine monitored alarms with leak detection, maintain roofs and gutters, and keep records of contractor work.

To balance premium and cash flow, you can sometimes accept a higher excess. Check endorsements, exclusions for outbuildings, and whether additional cover is available for materials stored on site during projects. When comparing insurance policies, weigh service quality and restoration expertise alongside price so support is there if a complex claim arises.

How to compare policies and choose the right cover

Set clear priorities before you obtain terms. Decide whether you need worldwide cover for personal items, broader accidental damage, and a claims pathway that understands heritage materials, then compare the policy wording on pairs and sets, alternative accommodation limits, and how outbuildings, pools and tennis courts are treated; if you prefer one contract, confirm how combined schedules work in your home insurance.

Review who is insured across the household and how new purchases are added mid term. Ask whether the schedule will provide cover for valuables kept in safes and whether automatic cover applies for gifts in peak seasons; if you commission custom work, check how the insurer treats materials stored on site and whether they offer cover for contractors’ liability in your home.

Worked example: calibrating a townhouse schedule

You have recently bought a four storey townhouse with bespoke joinery and a garden studio. A surveyor confirms a buildings sum insured that far exceeds the mortgage valuation, which is normal for central areas. You select high value home insurance with worldwide cover, wide accidental damage and alternative accommodation that keeps your children in their schools.

You itemise high value contents and fine art, add property emergency cover, and choose a slightly higher excess to balance cost. Because you host paying guests in summer, the insurer sets clear liability conditions. You also install a LeakBot under a free leakbot offer so water leaks are caught early and any cover loss is minimised.

The provider confirms additional cover for new purchases, how an entire set is treated, and who is insured across the household. The schedule documents specialist trades for heritage finishes so restoration standards are understood. This gives practical protection if you ever need to make a complex claim.

rivr: high value home insurance built around you

rivr is a high-value, digital-first home insurance provider built around the needs of modern lifestyles.

We provide tailored home insurance with clear limits, add ons, and support to make a claim when needed.

Speak to our team today to find the right level of contents cover for your home and lifestyle.

Read more

Frequently asked questions

It is a specialist home insurance arrangement for high value homes. It widens limits and home insurance cover across buildings and contents, often including worldwide cover and broader accidental damage. Standard home insurance usually sets lower single item limits, with policies that may exclude bespoke finishes unless optional sections are added.

Use a professional rebuild estimate for buildings and list contents at replacement as new. Index linking helps between reviews, but large homes benefit from fresh valuations after market shifts or renovations.

Rivr includes worldwide cover for your possessions. Losses while travelling are covered within policy limits, but items lent to people outside your household may not be. Always check your schedule for territorial and security conditions.

Often yes. Cover at rivr includes a 24/7 property-emergency helpline with call-outs up to £1,500 per incident, plus up to 36 months of alternative accommodation cover if an insured event makes your home uninhabitable.

Always insure your buildings for the full rebuild cost, not the market value. Include demolition, debris removal, professional fees, and compliance costs so your policy can fully settle a major claim.

Yes. Multiple properties can be listed on one policy schedule, with each treated as separately insured.

Currently, rivr only covers your main residence, but we will be bringing out multi-property cover soon. Watch this space!

Use the government long-term flood risk service and Historic England’s Listed Building Consent guidance.

The cost of high-value home insurance depends on a number of factors such as the level of cover you choose and specific risks associated with your property, like flood or theft.

Premiums are generally higher than standard insurance due to the increased value insured, but they provide broader protection, higher limits, and more comprehensive cover than standard policies.

Around £55,000. If your contents sum insured is set lower than the true replacement value, your payout could be reduced at claim time.