.jpg)

Building Insurance vs Home Insurance? Differences Explained

Is building insurance the same as home insurance? No. Buildings insurance covers your property's structure. Home insurance is an umbrella term for policies that typically cover both the building and your belongings. This guide explains what each covers, who needs which type, and how to choose the right policy before disaster strikes.

We'll also cover common exclusions, how to calculate your home's rebuild cost, and where home contents insurance fits in.

Understanding what insurance covers matters when assessing your coverage needs. rivr's buildings insurance policies include up to £3 million rebuild costs cover.

What buildings insurance covers

Building insurance covers your home's structure from specific risks. Buildings cover pays for repairing damage from events like fire or storm. Contents insurance covers your personal belongings separately.

What's covered and what isn't

This table shows what buildings insurance covers damage from under standard policies. Significant exclusions apply, including gradual damage, wear and tear, and certain subsidence types. Read the full policy wording and IPID before purchase.

Buildings, contents, or both?

Buildings insurance protects the structure of your home: roof, walls, floors, fitted kitchen and bathroom, outbuildings, and permanent fixtures.

Contents insurance covers your personal belongings: furniture, electronics, appliances, clothing. Your own possessions need separate protection from the building itself.

Most homeowners need both types of insurance policies. If you have a mortgage, buildings cover may be legally required. Tenants in a rented property need contents insurance only. Landlords need landlord building insurance for the structure, plus contents cover if the property is furnished.

Combined buildings and contents vs separate policies

A combined policy covering building and contents insurance protects both your property and your belongings. Combined buildings and contents insurance policies vary, so check the limits and exclusions match your coverage needs.

For listed buildings or high value items, separate insurance policies give you more control over the right cover. rivr offers standalone contents insurance policies with coverage for high value items. Policy limits and terms vary.

What buildings insurance protects against

Standard buildings cover includes damage caused by:

- Fire

- Flood and natural disasters

- Storm

- Vandalism (when occupied)

- Subsidence (strict conditions apply)

- Burst pipes

Optional extras on many insurance providers' policies:

- Accidental damage cover (protects against accidental damage from everyday mishaps)

- Alternative accommodation cover (if your home becomes uninhabitable)

- Legal expenses

- Home emergency cover

- Personal possessions outside the home

Holiday homes or properties left unoccupied for extended periods need specialist insurance policies.

Understanding rebuild costs

Buildings cover is based on rebuild costs, not market value. Your home's rebuild cost is the full cost of reconstructing your property from scratch: materials, labour, professional fees including architects fees and surveyors' fees, debris removal, legal fees, and compliance costs.

The cost of rebuilding is usually lower than your home's market value. Your home insurance policy must reflect the current rebuild cost. Underinsurance leaves you exposed.

Who arranges cover?

- Homeowners: Both buildings and contents insurance

- Landlords: Landlord insurance for the rented property structure. Contents insurance if furnished

- Tenants: Contents insurance for their own possessions in the rented property

Case study: Simon's unoccupied property claim

Understanding policy exclusions matters. This real case shows what happens when you don't.

Fire damaged Simon's property during renovation. His insurer refused the claim, citing an unoccupied property exclusion. The damage caused by fire should have been covered, but the unoccupancy exclusion applied.

What this shows:

- Buildings insurance often excludes damage caused if a property is unoccupied beyond the policy limit (usually 45 consecutive days)

- "Unoccupied" definitions vary by insurer

- Contents insurance policies cover possessions, not building structure

- Tell your insurer before leaving the property vacant for extended periods (more than 45 consecutive days)

How to calculate your home's rebuild cost

Your home's rebuild cost is essential for adequate cover. Here's how:

- Check your property details: Deeds or mortgage documents list your home's size and construction

- Use a rebuild cost calculator: Free online tools from insurers and industry bodies

- Get professional advice: For unusual or listed properties, use a surveyor

To get an accurate figure:

- Use a rebuild cost calculator (e.g. BCIS)

- Or ask a chartered surveyor for non-standard properties

Buildings insurance is based on rebuild costs, which is usually lower than market value.

Choosing the right policy

Get the right level of cover

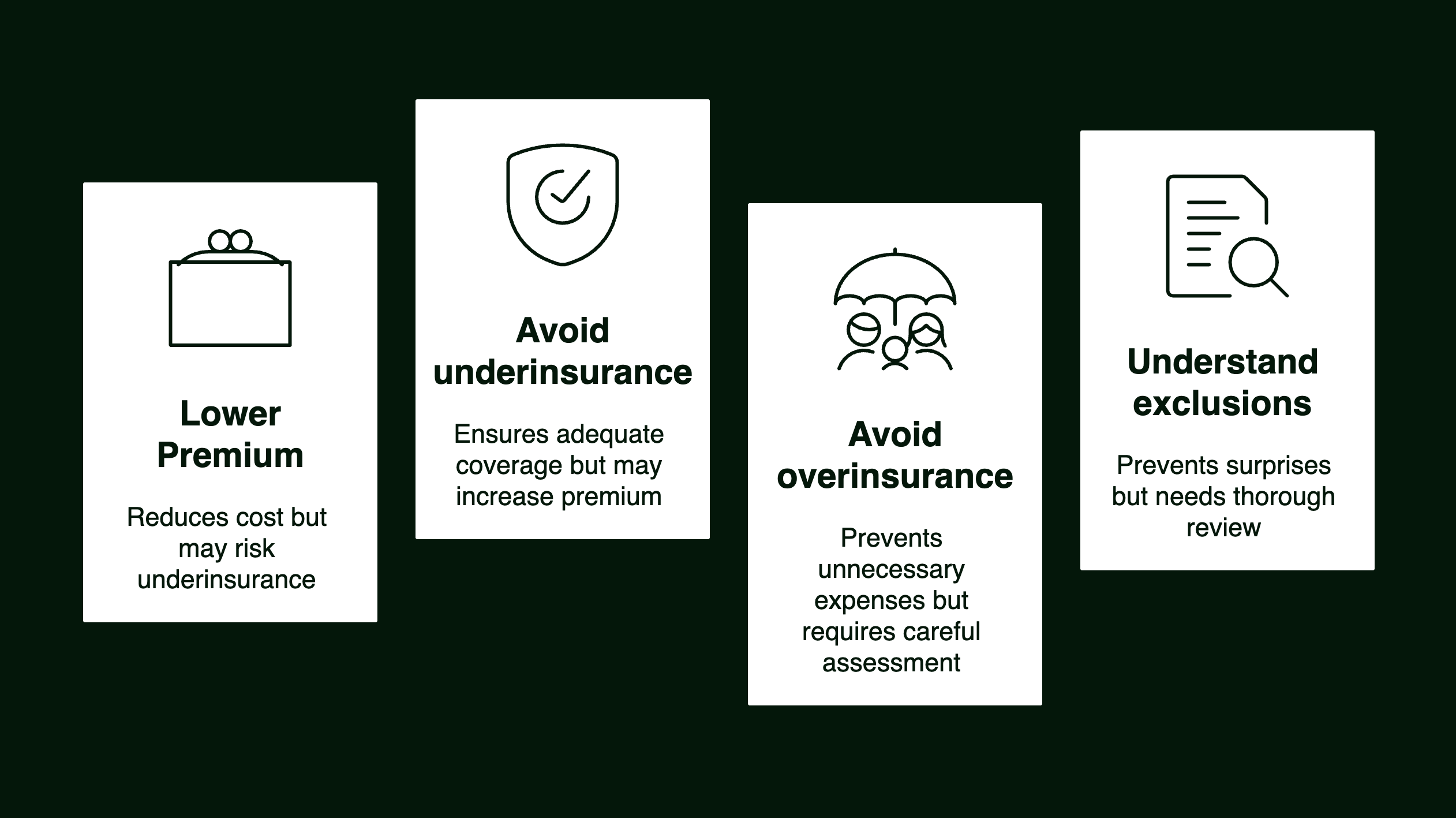

Several factors affect your coverage needs: property type, risk profile, and rebuild costs. The cheapest option isn't always the right insurance. Choose comprehensive cover that matches your situation to insure your property properly.

Lower your premium without cutting protection

Review your home insurance policy yearly, especially after home improvements or large purchases. Approved security features (smart alarms, CCTV, reinforced locks) reduce your premium without compromising protection.

Increase your voluntary excess (the excess amount you pay towards a claim) to avoid higher premiums. Only do this if you can afford the excess amount when you claim.

Bundling insurance policies (home and car) often gets you discounts. A no-claims bonus and Neighbourhood Watch membership can also reduce your premium.

Get the valuation right

Underinsurance leaves you exposed. Overinsurance means paying too much. Use online rebuild cost calculators and inventory your contents to ensure adequate cover.

Know what's excluded

Standard home insurance policies don't cover:

- Wear and tear or gradual deterioration

- Neglect or poor maintenance

- Pest or infestation damage

- Pre-existing damage

- Homes left unoccupied for extended periods (more than 45 consecutive days) face major coverage restrictions. Fire and storm remain covered, but theft, vandalism, escape of water (unless specific conditions are met), and accidental damage are excluded.

If anything is unclear, contact your insurer. Listed properties or homes in flood zones need specialist cover. Check what structural damage your home insurance policy covers.

Checklist: choosing the right home insurance

rivr: tailored policies for high value buildings

We insure high-value properties, listed buildings, and high value items with cover up to £3 million. Clear terms, expert support, the right cover for your coverage needs.

Contact us today for a quote.

Read more

Frequently asked questions

It depends on the repair cost and your excess. Minor cosmetic issues may not justify a claim, but significant structural damage usually will. Always check your policy and think about long-term costs before deciding.

No. Buildings insurance covers only the physical structure of a property, including walls, roof, and permanent fixtures. Property owners insurance includes buildings cover but also protects landlords against risks like loss of rent, legal liability, and damage to landlord-owned contents. It is designed for those renting out property, not just owning it.

Buildings insurance covers damage to the structure of a property, including risks such as fire, flood, or subsidence. Whereas indemnity insurance protects against legal or documentation issues, such as missing planning permission or access rights. It is typically arranged during property transactions to cover historic risks identified during conveyancing.

There is no fixed price. It depends on your rebuild cost, postcode risk, property type, claims history, security, excess, and any add ons. Many UK policies cost tens to a few hundred pounds a year, but higher risk homes can cost more. The quickest way to estimate is to get a few like for like quotes using the same rebuild value and excess.

Yes. You can buy buildings insurance whether you have a mortgage or not. If you own your home outright it is still worth having because it protects the structure. If you are leasehold the freeholder or managing agent often arranges buildings insurance for the whole building, so you may already be covered for the structure.

Sometimes. It usually covers sudden damage from insured events such as storms, fire, vandalism, or impact. It usually does not cover wear and tear, poor maintenance, or gradual leaks. If the damage is covered, the policy typically pays to repair the damaged area and any resulting internal damage, not a full roof replacement just because it is old.

Your payout can be reduced. Many insurers apply a proportional reduction if your sum insured is lower than the true rebuild cost. For example, if you insure for half the rebuild cost the insurer may only pay about half of a claim, minus the excess. You may also be left paying the shortfall after a major loss, so it is important to insure for an accurate rebuild cost and update it after renovations.

You may need high-value home insurance if your property or possessions exceed standard cover limits. Generally, this usually applies if:

- The rebuild value of your home is over £1 million.

- Your general contents are worth more than £100,000.

- Your valuables (such as jewellery, watches, or art) total more than £30,000.

High-value home insurance is designed to provide broader protection and flexible limits for clients with higher rebuild costs and collections of valuable items.